QuickScan: The PBoC’s Optimistic Outlook

In our latest QuickScan, we dissect the PBoC’s monetary policy report and outlook for the macroeconomy for the second half of the year. While the central bank paints an optimistic picture, there are a few catches.

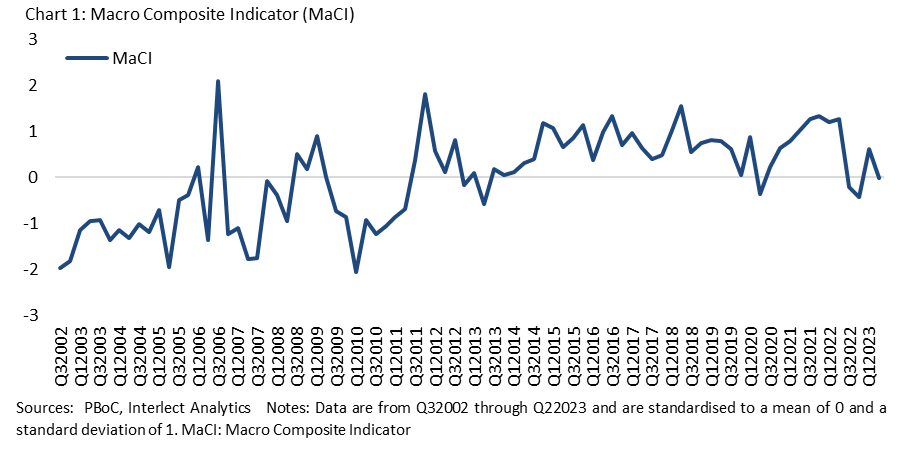

In its Q2 monetary policy report released last week, the People’s Bank of China (PBoC) largely painted a rosy picture for the macroeconomy in the second half of the year. It pointed to improving demand, business morale and purchase manager confidence, as well as strong investment growth in high-tech, new energy and infrastructure, arguing that these should give the economy a boost in the remainder of the year. The PBoC’s optimism is reflected in our text-based Macro Composite Indicator (MaCI), which fell when applied to the report’s outlook chapter.

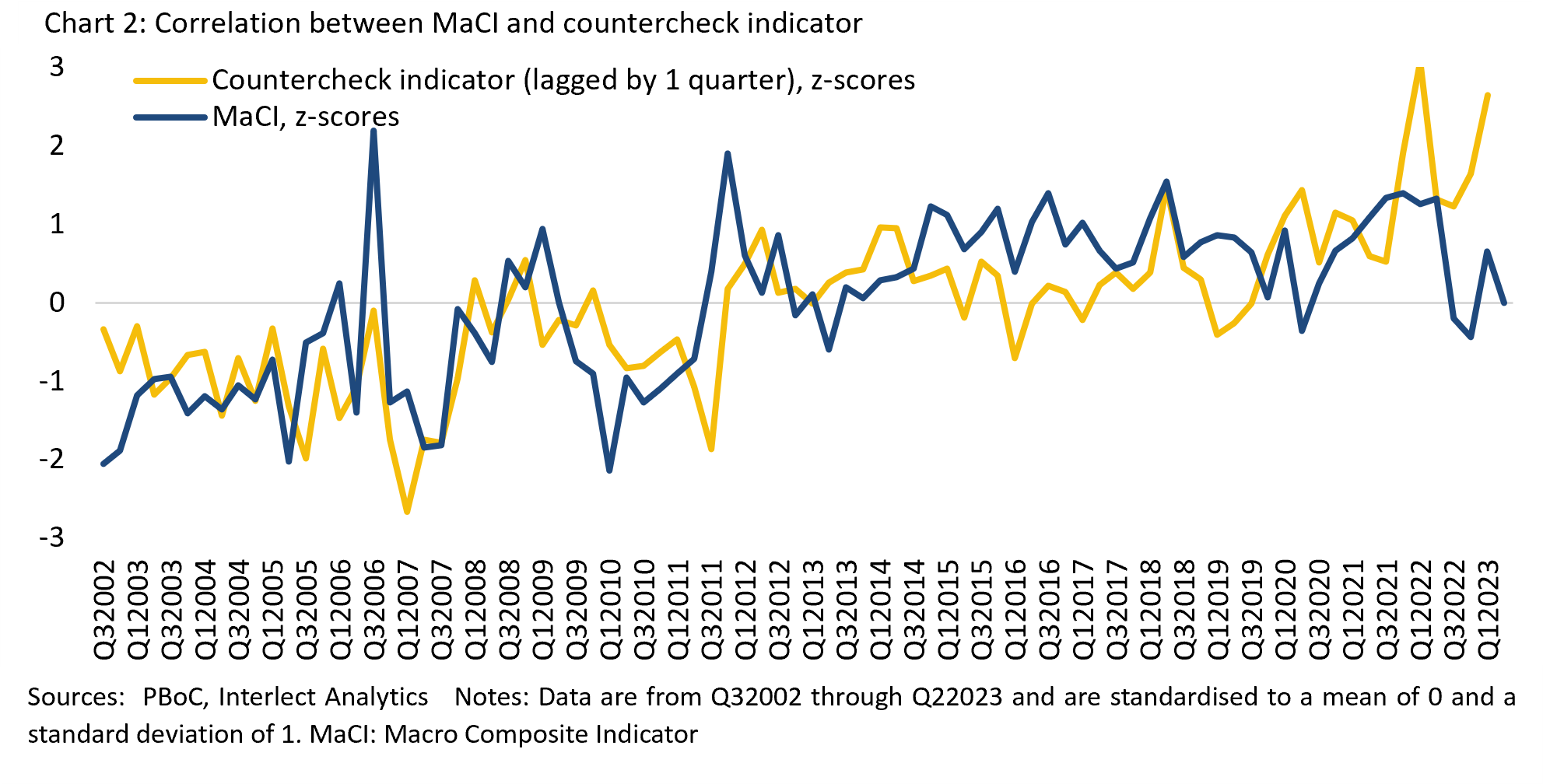

One caveat, however, is that our countercheck indicator, which can be used to cross-check or verify the results of the MaCI, continues to diverge from the MaCI. The index responds to topics that signal that more support is needed to prop up the economy and sentiment. The logic here is that a rise in references to risk and sluggish or worsening economic activity (MaCI increases) should overall co-occur with an increase in language signaling support for the economy (support indicator increases). Improving activity, on the other hand, should lead to a reduction in the use of such language. The MaCI and the countercheck indicator are positively correlated, with the former typically leading the latter by one quarter (cross-correlation of 0.6 at k = 1).

The MaCI and the countercheck indicator moved further apart in the PBoC’s Q2 monetary policy report, with the spread being one of the widest going back to 2002. The spread’s magnitude of 2.7 standard deviations makes us rather skeptical as to whether the economy is truly picking up.

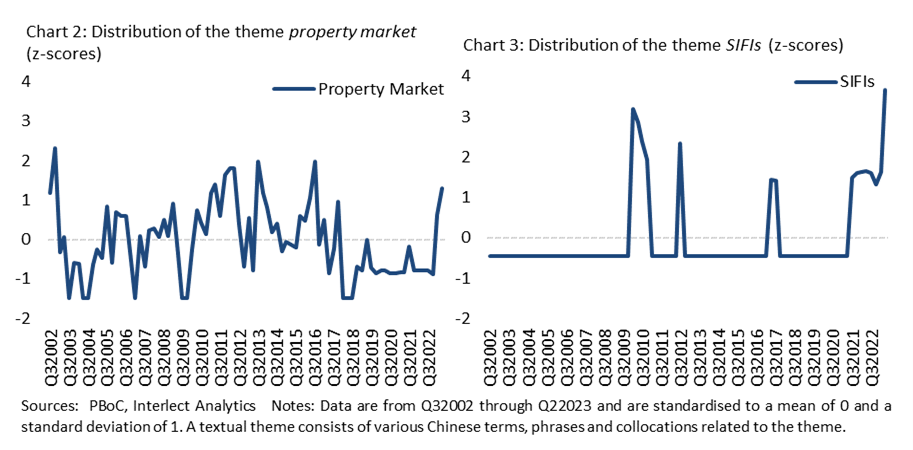

What also caught our eye is that the PBoC significantly upped its focus on systemically important financial institutions (SIFIs). It called for improved supervision of China’s global systemically important banks (G-SIBs) and asked them to strengthen their total loss absorption capacities (TLAC). In a first, the central bank also argued for the need to have better methodologies to assess systemically important insurers (SIIs) and proposed drafting additional regulatory requirements. The timing is unlikely to be a coincidence. Banks, insurers and trust companies have recently come under scrutiny due to their exposure to growing stress in the real estate market.

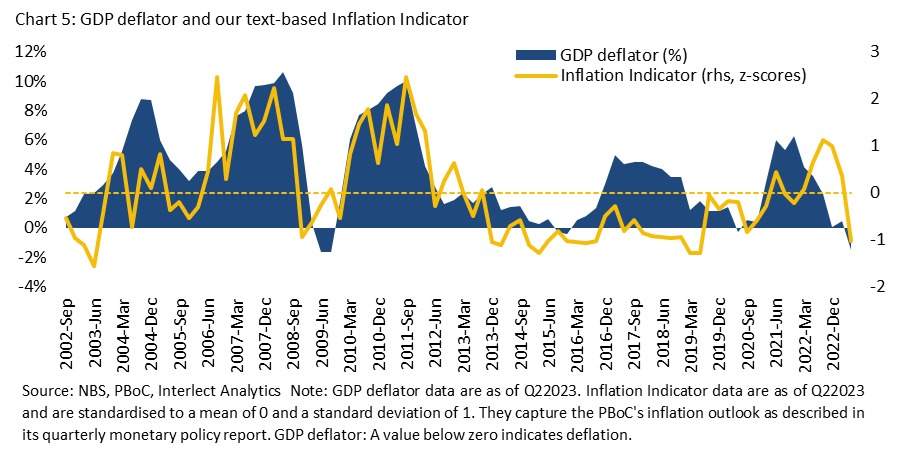

The PBoC held firm to its view that consumer prices have likely bottomed out, expecting a U-shaped trajectory for the rest of the year. We currently see little inflationary pressure due to continued slack in the jobs market, low demand and confidence, and falling import prices. This seems to be confirmed by the GDP deflator, although the core CPI increased 0.80 percent year-on-year in July, up from 0.4 percent in June. Our text-based Inflation Indicator, which responds to concerns over inflationary risk, remains subdued across statements and texts by different government agencies.

----------

This report has been prepared by Interlect Analytics Pte. Ltd. It should not be taken as investment advice or a recommendation to buy or sell any security or investment product. Redistribution without prior consent is prohibited.